NPS vs UPS has become one of the most discussed topics among Central Government employees after the introduction of the Unified Pension Scheme (UPS). Employees covered under the National Pension System (NPS) are evaluating whether UPS offers better retirement benefits and financial security.

The Government of India introduced UPS as an alternative framework under the National Pension System to provide greater pension certainty for eligible employees. As a result, lakhs of government employees are now comparing NPS vs UPS to understand which option is more beneficial for retirement planning.

This comprehensive guide explains the major differences between NPS and UPS, their benefits, eligibility criteria, pension calculations, and factors employees should consider before choosing either option.

What is NPS?

The National Pension System (NPS) is a contributory pension scheme introduced by the Government of India for central government employees joining service on or after January 1, 2004.

Under NPS:

- Employees contribute a portion of their salary.

- The government also contributes to the pension account.

- Funds are invested in market-linked instruments.

- Pension benefits depend on investment performance.

- Retirement corpus accumulates throughout service.

NPS was designed to create a sustainable retirement system while encouraging long-term savings among employees.

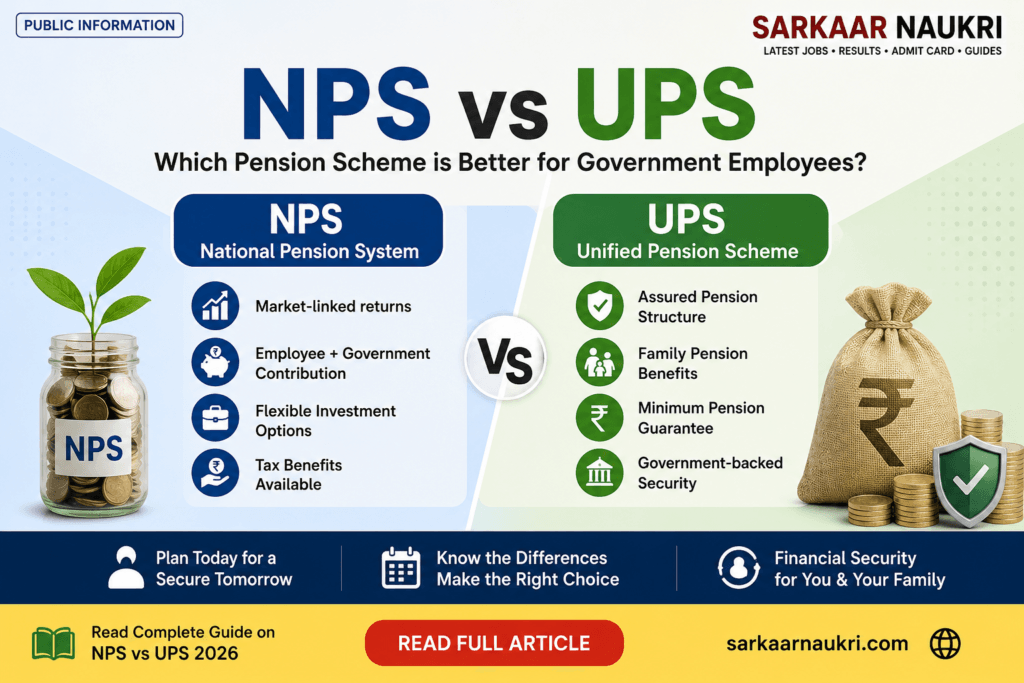

Key Features of NPS

- Market-linked returns.

- Individual pension account.

- Government contribution available.

- Portable across jobs.

- Flexible investment options.

- Tax benefits under applicable provisions.

The retirement corpus under NPS is influenced by market performance, making returns potentially higher but also subject to investment risk.

What is UPS?

The Unified Pension Scheme (UPS) is a pension framework announced by the Government of India for eligible Central Government employees covered under NPS.

The primary objective of UPS is to provide more predictable retirement benefits and greater financial security after retirement.

UPS introduces a structured pension assurance mechanism that differs significantly from the market-linked nature of NPS.

Key Features of UPS

- Assured pension structure.

- Retirement income security.

- Government-backed pension framework.

- Family pension benefits.

- Minimum pension provisions for eligible employees.

- Continued operation within the broader NPS architecture.

The introduction of UPS aims to address concerns regarding uncertainty in retirement income under the traditional NPS model.

NPS vs UPS: Major Differences

Understanding NPS vs UPS requires examining the core differences between the two systems.

| Feature | NPS | UPS |

|---|---|---|

| Pension Type | Market-linked | Assured Pension |

| Risk Level | Depends on market performance | Lower uncertainty |

| Retirement Benefits | Based on corpus accumulated | Based on defined pension formula |

| Pension Predictability | Variable | More predictable |

| Government Contribution | Available | Available |

| Family Pension | Available through provisions | Structured benefits |

| Minimum Pension | Not guaranteed in traditional structure | Available under specified conditions |

This comparison highlights why many employees are closely analyzing NPS vs UPS before making retirement-related decisions.

Pension Benefits Under NPS

Under NPS, retirement benefits depend on:

- Employee contributions

- Government contributions

- Investment returns

- Duration of service

- Market performance

The final pension amount can vary significantly among employees.

Advantages of NPS

1. Higher Growth Potential

Since investments are linked to market instruments, employees may accumulate a larger retirement corpus over time.

2. Investment Flexibility

Employees can choose investment preferences based on risk appetite.

3. Tax Benefits

NPS provides several tax-saving opportunities under applicable income tax provisions.

4. Portability

The account remains portable even when changing departments or locations.

Limitations of NPS

- Pension amount is not fixed.

- Market fluctuations affect returns.

- Retirement income may vary.

- Financial planning can be challenging due to uncertainty.

Pension Benefits Under UPS

UPS focuses on retirement income certainty.

The scheme seeks to ensure that eligible employees receive predictable pension benefits after retirement.

Advantages of UPS

1. Assured Pension

One of the biggest advantages of UPS is guaranteed pension support based on prescribed eligibility conditions.

2. Greater Retirement Security

Employees can plan retirement finances more effectively because future pension benefits are easier to estimate.

3. Family Protection

UPS includes provisions that provide financial support to family members after the employee’s death.

4. Reduced Market Risk

Retirement benefits are not entirely dependent on market performance.

Limitations of UPS

- Less flexibility compared to market-linked investments.

- Future modifications may depend on government policy.

- Employees seeking higher market-driven returns may prefer NPS.

NPS vs UPS: Which Provides Better Retirement Security?

When evaluating retirement security, UPS generally offers greater predictability.

Government employees often prioritize:

- Stable pension income

- Family pension protection

- Long-term financial security

- Inflation management

UPS addresses many of these concerns by providing an assured pension framework.

However, employees comfortable with market investments may still find NPS attractive due to its potential for higher returns.

NPS vs UPS: Government Contribution Comparison

Both systems involve government contributions.

Under NPS:

- Government contributions are invested alongside employee contributions.

- Final benefits depend on corpus growth.

Under UPS:

- Government support contributes toward maintaining the assured pension structure.

The exact financial impact depends on service length, salary progression, and retirement conditions.

NPS vs UPS for Young Employees

Young employees often have a long investment horizon.

For such employees:

NPS Advantages

- More time for investments to grow.

- Higher potential corpus accumulation.

- Ability to benefit from long-term market appreciation.

UPS Advantages

- Greater certainty.

- Less retirement anxiety.

- Guaranteed pension structure.

The choice depends on whether an employee prioritizes growth or stability.

NPS vs UPS for Employees Near Retirement

Employees approaching retirement generally focus on income security.

UPS may appear attractive because:

- Pension expectations become clearer.

- Market volatility becomes less concerning.

- Retirement planning becomes simpler.

For many employees nearing retirement, predictable monthly pension income is often more important than potential market gains.

Family Pension Benefits Under UPS

One of the important features discussed in NPS vs UPS comparisons is family pension support.

UPS provides structured financial protection for eligible family members after the death of a pensioner.

This feature enhances social security and reduces financial uncertainty for dependents.

Minimum Pension Benefits

Another major difference in NPS vs UPS discussions is minimum pension assurance.

UPS introduces provisions aimed at protecting retirees from extremely low pension outcomes.

This is particularly beneficial for employees concerned about inadequate retirement income.

Tax Implications of NPS and UPS

Both systems are subject to applicable government regulations and tax provisions.

Employees should consult:

- Income Tax Act provisions

- Official government notifications

- Financial advisors

before making retirement planning decisions.

Tax treatment may change through future policy amendments.

Who Can Opt for UPS?

Eligibility depends on government notifications and applicable service rules.

Generally, UPS is intended for eligible Central Government employees covered under NPS.

Employees should carefully review official notifications before exercising any option.

NPS vs UPS: Which is Better?

The answer depends on individual priorities.

Choose NPS if you prefer:

- Market-linked growth.

- Potentially larger retirement corpus.

- Investment flexibility.

- Long-term wealth creation.

Choose UPS if you prefer:

- Assured pension.

- Retirement income certainty.

- Reduced market risk.

- Better predictability.

There is no universally superior option. The best choice depends on an employee’s risk tolerance, financial goals, age, and retirement expectations.

Frequently Asked Questions (FAQs)

What is the main difference between NPS and UPS?

The primary difference is that NPS is market-linked, while UPS provides a more assured pension structure for eligible employees.

Is UPS better than NPS?

UPS may be better for employees seeking pension certainty, whereas NPS may be better for those seeking potentially higher returns.

Can government employees choose between NPS and UPS?

Eligibility and choice depend on official government guidelines and notifications.

Does UPS provide family pension?

Yes, UPS includes provisions related to family pension benefits for eligible beneficiaries.

Is NPS risky?

NPS carries market-related risk because retirement benefits depend on investment performance.

Conclusion – NPS vs UPS

The debate surrounding NPS vs UPS reflects the growing importance of retirement planning among government employees. While NPS offers market-linked growth and flexibility, UPS focuses on pension certainty and financial security after retirement.

Employees should carefully assess their risk appetite, retirement goals, and long-term financial requirements before making any decision. Reviewing official government notifications and consulting financial experts can help ensure the most suitable choice.

For employees who value stability and assured retirement income, UPS may be an attractive option. For those comfortable with market-linked investments and seeking potentially higher returns, NPS remains a strong retirement planning tool.